Mary Meeker: The State Of The Web, December 2012

December 25, 2012 Leave a comment

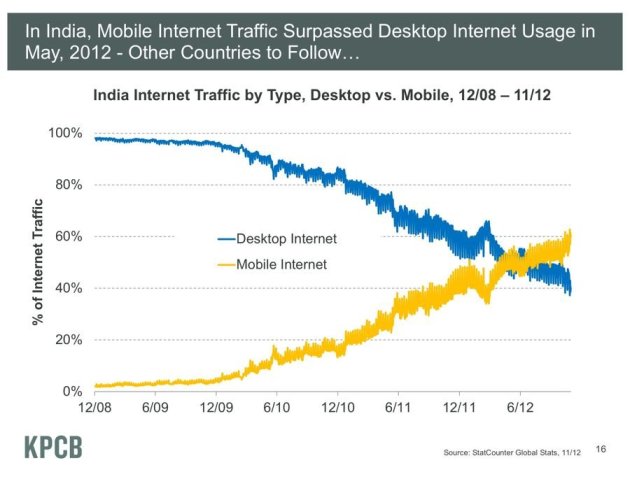

Mary Meeker’s Presentation On The State Of The Web December 2012

Sugar-Water Startups

November 11, 2012 Leave a comment

VC Overview

VC investors completed 685 investments in U.S.-based companies totaling $6.1 billion in 3Q 2012, dramatic drops from the levels achieved in 2Q 2012. The drop-off in dealmaking was not confined to a particular stage of the

investment cycle, as angel/seed, early, and late stage deal volume all fell by approximately one-third. It’s important to put this decline into context, as VC investment year-todate is still even with 2011.

The second quarter of 2012 registered the most VC financings of all-time for a single quarter, so a pullback should not be too alarming. Furthermore, activity had increased 30% from 4Q 2011 to 2Q 2012, which has led some to speculate that VCs took advantage of the summer months to recharge before a push at the end of the year.

VC deal flow has been on a general upward trajectory since the beginning of 2011, but the total amount of money invested through VC deals has been trending downward since 1Q 2011.

A contributing factor has been that angel and seed stage deals have grown from 17% of financings in 3Q 2011 to 23% in 3Q 2012, while the typically larger late stage financings have contracted from 36% to 31% during the same period.

On a yearly basis, it will be difficult for 2012 to surpass the record-breaking numbers posted in 2011. Still, deal-making has been strong despite the disappointing 3Q figures, and 2012 could still prove to be the second-best year for VC investments by both deal count and capital invested.

Industry Rundown

It should come no surprise that the IT industry accounted for the majority of VC investment during 3Q 2012, representing 50% of deal flow and 48% of the capital invested. The proportion of VC money flowing into the IT industry has steadily been rising since dipping to 33% in 2Q 2011 and now sits at its highest level since 3Q 2006.

One of the most significant trends in VC investing has been the increasing prevalence of deals being executed in the B2C space, particularly in the earlier stages. Since 1Q 2009, B2C has expanded from 14% of VC financings to 20% in 3Q 2012. Over the same period, B2C grew from 10% to 16% of capital invested. For the first time ever, B2C now accounts for a higher proportion of VC deals (20% through the first three quarters of the year) than the Healthcare industry (17%). However, Healthcare companies continue to attract significantly more

dollars as the bulk of the industry’s financings come in the later stages.

Renewable energy and clean tech are commonly thought of as a prime spaces for VC investment, but the data tell a different story. Investors closed just 16 Energy deals totaling $298 million in 3Q 2012, representing a measly 2% of deal flow and 5% of capital invested.

VC exits

At first blush, the quarterly exit numbers seem abysmal with a 75% drop-off in capital exited from 2Q to 3Q. However, the quarterly comparisons for exit activity are a bit muddled due to the $16 billion Facebook IPO in 2Q. With that deal removed, the decline in capital exited is a much more tolerable 8%. Still, exit volume did fall substantially from 113 deals in 2Q 2012 to 96 in 3Q. The outlook is much better when looking at the data on a yearly basis; 2012 has already broken the record for most capital exited with $35.5 billion and the final exit count should be on par with the two preceding years. Corporate acquisitions continue to be the exit method of choice for VC companies, but the exit strategy has fallen to 72% of activity, the lowest level since 2Q 2007. IPO activity declined slightly in 3Q, but 2012 has already seen 36 VC-backed IPOs, which is the highest total for the first three quarters of a year since 2000.

Private equity firms have increasingly been turning to the VC space to source deals and set a new record (42) for VC-backed company buyouts in the first three quarters of 2012.

While VC investment activity is driven by IT, the industry plays an even larger role when it comes to exits. IT companies have accounted for 57% of exit volume and 78% of the capital exited through the first three quarters of the year.

August 14, 2012 Leave a comment

Global economic malaise restrained the deal value global technology mergers and acquisitions (M&A) in the second quarter. However, steady deal volume reflected the ongoing drive of five disruptive technology megatrends — smart mobility, cloud computing, social networking, big data and cross-sector and cross-industry blur, according to Ernst & Young’s Global technology M&A update: April-June 2012.

“There were several surprises in the second quarter, with US buyers ’sitting out‘ a sequential increase in transaction value that was driven out of Europe, Canada and Japan,” explains Joe Steger, Global Technology Industry Transaction Advisory Services Leader at Ernst & Young.

That said, “Disruptive technology megatrends continue to fuel strategic deal-making around the world, in spite of a difficult economic context,” continues Steger. “In the second quarter, we even saw new sub-trends emerge to drive deals, such as alternative input technologies like speech and handwriting recognition.

So, while the current macroeconomic challenges may dampen the appetite for large, transformative deals in the near term, expect to continue to see smaller, strategic deals — especially in the technology megatrends. “And the long-term outlook for global technology M&A remains strong,” Steger concludes.

According to the report, resurgent macroeconomic uncertainty worldwide caught up to the technology industry, which had outpaced deal value for all industries in the first quarter of 2012 but fell behind in the second quarter. Nevertheless, global technology deal volume remained around the 730-deal average seen for the last six quarters.

The cloud/SaaS megatrend drove the highest volume and value of global technology transactions for the second consecutive quarter. There were four cloud-driven deals among the quarter’s top 10, including the purchase of a SaaS company that also hosts a web-based B2B business exchange, two deals in which companies outside of the technology sector are buying data centers to offer cloud services and another purchasing cloud hardware and software.

All five disruptive megatrends came together to drive dozens of advertising/marketing technology transactions in 2Q12, including several acquisitions by large global advertising firms. Big data analytics to understand customers’ and prospects’ social networking activity was key to many of these deals.

Other targeted technologies included marketing automation SaaS and tools for optimizing mobile and online campaigns.

At $28.9 billion, corporate aggregate deal value was down 37% YOY but increased 50% sequentially. Of note, the second quarter’s aggregate deal value YOY comparisons are with a 2Q11 that included many unusually large big-ticket deals, making for a tough YOY comparison.

“Disruptive technology megatrends continue to fuel strategic deal-making around the world, in spite of a very difficult economic context,” says Steger.

“In the second quarter, we even saw new sub-trends emerge to drive deals, such as alternative input technologies like speech and handwriting recognition, in addition to the convergence of “social-mobile-cloud” and big data analytics. The outlook for global technology M&A remains strong. But caution around executing large technology deals will persist in the near term until macroeconomic conditions improve.”

June 12, 2012 Leave a comment

Preqin Special Report: Venture Capital draws exclusively on the following sources of information:Venture Deals Analyst – The most extensive, detailed source of information on venture capital deals in the world.

This comprehensive product contains in-depth data for over 21,000 venture capital transactions across the globe and comprehensive portfolios for the top 50 VC firms. Deal profiles include information on value, buyers, sellers, financing, financial and legal advisors, exit details and more.

Investor Intelligence – The most comprehensive database of current and potential institutional investors in private equity, featuring in-depth profiles of more than 4,000 actively investing LPs, and over 1,000 that have put their investments on

hold, including investment preferences, future plans, key contact details and more.

Funds in Market – This constantly updated resource includes details for 1,850 funds of all types being raised worldwide, with key information on strategy, target sizes, interim closes, placement agents, lawyers, and LPs.

Fund Manager Profiles – With detailed profiles for over 6,250 GPs, including key strategic and investment preferences, Fund Manager Profiles is the foremost source of data on private equity and venture capital fund managers worldwide.

Performance Analyst – The industry’s most extensive and transparent source of net-to-LP private equity fund performance, with full metrics for over 5,800 named vehicles. In terms of capital raised, Performance Analyst contains data for over 70% of all funds raised historically.

February 29, 2012 Leave a comment

Dynamics for 2012 and beyond.

The global PE industry edged into the new year trailing heavy baggage from 2011 and surrounded by a dense fog of potentially destabilizing uncertainties. The US economy remains weak, hobbled by stagnant household incomes, anemic spending by over leveraged consumers, fi scal policy gridlock heading into an election year and hesitancy on the part of businesses to invest until the growth outlook clears. In the euro zone, policy makers have managed to improvise patchwork solutions that have held the currency union together, but the risk is real that a misstep could cause the fragile stability to unravel, with potentially catastrophic consequences for the banking sector and the global economy. Emerging markets and other major economies face uncertain prospects in 2012. China, an engine of global expansion throughout the downturn and since, is early in what could prove to be an unsettling transition as the economy, built around export growth, adjusts to reduced global demand for its goods and services. Meanwhile, natural resources-rich Brazil, Australia and Canada will ride the waves of volatility emanating from the US, Europe and China that consume their energy, minerals and other primary inputs. In short, PE investors will need to navigate a sea of global macroeconomic and geopolitical worries in a year characterized by choppy equity markets and nervous debt markets that could be capsized by any number of policy miscalculations or exogenous shocks.

January 12, 2012 Leave a comment

Amid the fragile economic recovery and highly volatile capital markets of 2011, the venture capital (VC) sector is becoming increasingly globalized. A shift toward the emerging markets

can be seen in geographic VC patterns and the growth of new global VC hotbeds. Although the United States will likely remain at the leading edge of VC-backed innovation for many years to come, US VC fund-raising continues its decade-long decline.

Elsewhere, in China, India and other emerging markets, vibrant innovation hotbeds and entrepreneurial talents are arising, and investors are focused on less risky, later-stage deals, at least for now.

Although unrealistic valuations may dampen future returns, China’s VC industry reached record heights in 2011 and will soon surpass Europe as the second-largest venture hub for

fund-raising in the world. Both China’s and India’s strong VC industries are expected to continue their rapid growth and development as they capitalize on strong GDP growth,

growing domestic consumption and a dynamic entrepreneurial ecosystem. At the same time, due to Europe’s sovereign debt crisis and its muted medium-term growth potential, Europe’s VC industry has lost some of its robustness.

Globally, companies are staying private longer, due to large corporations seeking proven business models prior to an acquisition and investors that prefer companies with a proven profitability path both before and after the IPO. As angel investors have become major investors in early-stage start-ups, particularly in the US, the competition has nudged VCs toward later-stage, high-growth ventures.

Broadly speaking, the more mature VC markets of the US and Europe favor earlier–stage investments, while the emerging markets of China and India generally prefer later-stage

companies. In China and India, IPOs represent the vast majority of exits for VC-backed companies. But in the US, Europe and Israel, the main exit route for VC-backed companies is

acquisitions (M&A), representing more than 90% of all exits.

Furthermore, VC fi rms are also selling companies to private equity fi rms as a third path to liquidity.

Contrary to the popular perception that global VC investment has been concentrated primarily in the frothy digital media sector, VC funding has been quite evenly spread across sectors and life-cycle stages and has progressed at a reasonable pace.

Worldwide, the VC universe continues to shrink as limited partners focus on top performers or forego VC altogether.

However, the sector’s continued long-term consolidation is viewed as good for the sector, with fewer players investing smaller amounts in companies that will reach profitability faster

than they do today. Large corporations striving to maintain market leadership are partnering with VC fi rms to access external innovation and a pipeline of new products and services.

This report explores these themes in articles and interviews, including:

• Interviews with top VC investors and entrepreneurs from

around the globe

• “Paradigm shifts in venture capital,” our keynote article with

insights on VC investment, IPO, M&A and valuations, based on

data from 2005 to 2011

• Key trends in the global digital media and biotechnology

sectors and from global corporate venturing

• An in-depth analysis of the key global VC hotbeds of the US,

China, Europe, India and Israel

September 20, 2010 Leave a comment

International_PE_VC_Valuation_Guidelines_Edition_August_2010

February 14, 2010 Leave a comment

Due diligence in the venture industry is the investigation and analysis the investor performs to see if an investment opportunity meets the investor’s criteria for funding. For angels as well as venture capitalists, the primary objective of due diligence is to mitigate investment risk by gaining an understanding of a company and its business as well as determining the suitability of the investment for the portfolio.